History in the making

As events unfold, it can be difficult to parse out what will make it into the history books and what will be consigned to the ash heap. Only with the benefit of time do things become clear and sometimes, even with the benefit of centuries, it can be ‘too early to say’[1]. 2024 was certainly an eventful year encompassing further market excitement around the AI narrative, major elections and ongoing military conflicts.

The performance of the strategy, at just under +7%, is in line with its long-run average. In a year in which the FTSE All-Share returned +9.4%, the MSCI World Index was up +21.5% and UK CPI was up +2.5% we believe this was an acceptable but not exceptional return. Gold, the single largest contributor to returns, appreciated +30% in sterling terms. Its performance was underpinned by another year of strong central bank buying and ‘de-dollarisation’ as central banks, particularly in Emerging Markets, continue to shift their assets away from the dollar. Geopolitical fissures will likely continue to widen as nations move their centres of gravity away from the West.

Meanwhile, our equities contributed strongly. This came from a range of stocks, with Unilever the strongest contributor followed by good returns from the payments networks, and other technology businesses such as Microsoft and Alphabet.

For US stock markets, the past two years have been dominated by Artificial Intelligence, leading to stark outperformance versus other markets and much talk of US exceptionalism. The ‘Magnificent Seven’ stocks (comprising Apple, Nvidia, Microsoft, Alphabet, Amazon, Meta and Tesla) generated returns of +107% in 2023 and +67%[2] in 2024. The enthusiasm around AI’s potential is facilitating huge infrastructure investment and laying the foundations for a technology that is likely to have profound significance beyond its recent impact on share prices. Bill Gates said in 2022, ‘In my lifetime, I’ve seen two demonstrations of technology that struck me as revolutionary. The first time was in 1980, when I was introduced to a graphical user interface…The second, from OpenAI.’

Longstanding investors in Troy’s multi-asset funds will be unsurprised to discover that the portfolio does not hold semiconductor stocks, the companies at the epicentre of recent excitement. Our aversion to high degrees of cyclicality and volatility makes these companies less appropriate for us in pursuing our objectives. We nonetheless respect and are fascinated by the value created by the likes of Nvidia, whose share price has appreciated +680% in the past two years, following a drawdown of -66% as recently as 2022. Given the magnitude and far-reaching nature of AI, it is incumbent upon us as investors to seek to understand what the technology might mean for the economy, asset prices and the businesses in which we invest. We expect that the details of this will take shape over a number of years.

Already, the adoption and monetisation of AI is occurring faster than previous technological shifts. This is thanks in large part to the pre-existence of the internet as infrastructure, underpinning the development of AI and the distribution of its applications. Of ChatGPT’s c. 300m weekly active users, >10m already pay a monthly subscription. This differs from the advent of the internet itself when investors had little more to go on than ‘clicks and eyeballs’ at the time of the dot-com boom.

This increasing shortening of the lag between technological invention and mass adoption is striking. The telephone was first patented in 1876. In large part due to the physical network that needed to be built, it took until 1945 for 45% of US households to own one.

Whilst large language models (LLMs) are already strikingly impressive across a number of applications, from writing essays to servicing customers, the technological potential and scale of adoption remain nascent versus the opportunity. At the time of writing however, a step change in the cost of training and consuming models is occurring. This points to the potential for the limits on this technology’s efficiency and availability to be lifted. Those technology companies with the greatest distribution stand to benefit. In the words of Microsoft’s CEO Satya Nadella, ‘we will see its (AI’s) use skyrocket, turning it into a commodity we just can’t get enough of.’ We own both Microsoft and Alphabet, whose valuations have not risen in the past 18 months even as the rest of the market has re-rated. Microsoft and Alphabet’s existing cloud businesses should continue to benefit as customers who seek access to computing power, in order to run LLMs, leverage their infrastructure.

Animal Spirits

Every bubble has two components: an underlying trend that prevails in reality and a misconception relating to that trend.

George Soros

Whilst the market is right to identify change, it can also be quick to judge and reward as yet unknowable returns. Many of the conditions present in markets today have echoes of prior bubbles. And whilst we expect that we have not yet reached ‘irrational exuberance’ when it comes to market sentiment, we may well be on our way. The fact that Alan Greenspan coined the term ‘irrational exuberance’ to describe sentiment in December 1996, over three years before the dot-com bubble burst, demonstrates the difficulty in timing behavioural shifts. The revenues that result from AI will occur unevenly and it is likely that the market, having priced for the potential, will become impatient for delivery along the way.

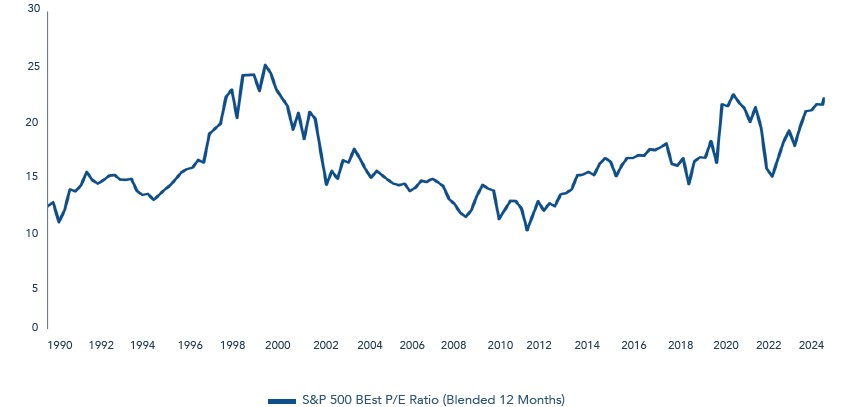

One characteristic of the US stock market today, in common with past bubbles, is the narrowness of its leadership. At the end of 2024, the top seven companies constituted just under 34% of the S&P 500 index. Concentration across a handful of stocks reflects fragility to the extent that markets are vulnerable when sentiment towards those companies reverses. It is no coincidence that previous peaks in concentration (1964 and 1999) preceded multi-year bear markets. In terms of market sentiment today, various warning lights are flashing orange if not red. Survey data shows fund managers running cash levels near all-time lows whilst also highlighting that US households have not been so bullish on the fortunes of the US equity market since at least 1987. Meanwhile, when it comes to fundamentals, valuations are high. The S&P 500 index trades on 22x forward earnings, which is almost as expensive as the peak reached in 2021, but below that of 2000 (see Figure 1).

FIGURE 1 – S&P 500 BLOOMBERG ESTIMATED P/E RATIO (12-MONTH FORWARD EARNINGS)

Source: Bloomberg, 23 January 2025. Past performance is not a guide to future performance.

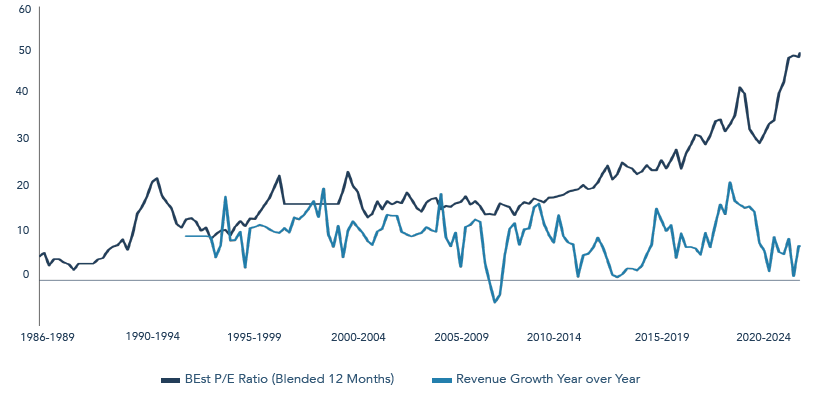

This said, there is nuance beneath the surface. The top seven companies in the US by market capitalisation are in aggregate more expensive than the index average but, within the group, wide divergences exist. Alphabet trades below the average valuation of the market whilst Tesla trades on 130x earnings. And although the largest businesses garner the most attention, only two out of the seven actually sit within the top fifty most expensive stocks in the index. The other 48 are comprised predominantly of technology businesses but there are signs of excess far beyond the theme of AI. From the ascent of Donald Trump’s meme coin to over $10bn in a weekend (before Melania stole the limelight with her own), to the number of relatively predictable businesses trading on elevated valuations, animal spirits are everywhere. Costco, a business which has enjoyed many years of consistent mid to high single-digit growth (and a mid-teens boom post-pandemic), at low margins of 2.5-3.5%, is now valued on 50x earnings, over double that of a decade ago (see Figure 2). Whenever company valuations enter a ‘new normal’ phase, without commensurate improvement in their fundamentals, scepticism is warranted. The psychology behind bubbles is intuitive. Investing is more art than science and there is subjectivity in every valuation, leaving room for stories to take hold.

FIGURE 2 – COSTCO VALUATION AND SALES GROWTH

Source: Bloomberg, 23 January 2025. Past performance is not a guide to future performance.

All discounted cash flow calculations are highly sensitive to small changes to their inputs. Meanwhile, when your neighbour is making money, the temptation is to join in. The S&P 500 is the gift that keeps on giving, so why question it? The experience of the Nifty Fifty stocks in the late ‘60s and early ‘70s is instructive. Often touted as ‘one decision’ stocks, these c. 50 companies traded on ever-higher valuations owing to their perceived predictability against a backdrop of rising inflation. This worked until it didn’t, with most of the companies involved experiencing a multi-year bear market in the years that followed.

Who’s afraid of the big bad wolf?

I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.

James Carville, political adviser to Bill Clinton

Any period of excess is followed by a period of calibration, but it is rarely clear ahead of time what will trigger a return to rationality. We have been surprised by the failure of higher bond yields, so far, to exert their gravitational pull over equities. We suspect that if earnings growth continues to be strong, stocks will ignore the repricing of the risk-free rate that has occurred since 2021. It is often not until the fundamentals begin to disappoint that holders really start to question what valuation they are prepared to pay.

The yield on the US 10-year Treasury bond has risen from 3.6% to 4.6% since September. Over the same time frame the UK 10-year yield has also risen to 4.6% today, having hit 4.9% earlier this month, its highest level since the Financial Crisis. There are common themes affecting both. In the US, yields began to rise as soon as a Trump election victory became more likely. His policies, when it comes to immigration and tariffs, are feared for their inflationary ramifications whilst the spectre of ongoing fiscal laxity raises the question as to how long bond markets will tolerate current levels of debt to GDP (gross domestic product). This latter point is true also of the UK. We expect that volatility in longer-duration bonds is likely to continue in the face of such largesse.

At the same time, expectations for shorter-term interest rates have also shifted, as the Federal Reserve (the Fed) has lowered market expectations for rate cuts in 2025. The market has gone from pricing in over five rate cuts as recently as September, to around one rate cut today. This has been in response to a stronger than expected economy, and the risk of stronger inflation. The equity market is certainly pricing in a soft landing, and valuations suggest small scope for disappointment. Whilst we have been surprised so far by the resiliency of the US economy in the face of higher interest rates, we remain open-minded as to whether a soft landing is secure. We expect there will be more shoes to drop. With Germany experiencing two consecutive years of GDP decline, the UK limping on in 2024 after a recession end-2023 and China’s growth slowing, the rest of the world may start to impact on its largest economy. Meanwhile, domestically, the US commercial real estate market, estimated to be worth $23trn at the end of 2023, continues to show signs of stress. According to rating agency Fitch, commercial real estate problem loans are approaching Global Financial Crisis levels. This is of particular relevance to smaller banks in the US which are most exposed.

Selective opportunities

The picture is mixed, and we must embrace the nuances. Big shifts, like the one we are currently witnessing in AI will disrupt existing business models whilst presenting vast opportunities for value creation. The valuations of hoped-for beneficiaries are likely to soar long before the winners and size of the prize are known. Amidst the excitement, companies that fail to capture the zeitgeist with a compelling story will be overlooked, creating opportunities for long-term investors. This was the case for many defensive companies, perceived to be boring, during the dot-com era. We suspect that what is occurring will continue to draw investors into more speculative areas, lured by the prospect of outsized returns. That is appropriate for venture capital but not for our investors, who sit at the opposite end of the risk spectrum. We will be led by company fundamentals and valuations, combined with an understanding of directional change. Our equity exposure remains modest at c. 30%, and we will continue to lean into opportunities thrown up by an impatient or distracted stock market. In the rest of the portfolio, higher yields in fixed income are enabling us to reinvest maturing bonds at higher rates of return. Such has been the benefit of holding modest duration in today’s rate environment.

Vale

Turning to Troy’s business, our longstanding Chairman Jan Pethick will be retiring at the end of March. Jan’s entrepreneurial energy and warm charisma, combined with his depth of experience and market nous, will be much missed. We are however delighted to announce that Francis Brooke, current Executive Vice-Chairman and longstanding member of the Board, will be taking over as Non-Executive Chairman. Francis’s knowledge of the business and our people, combined with his long and successful career as a fund manager, makes this appointment a natural one. In order to ensure a smooth transition, Jan will remain on the Board as a non-executive director until the end of 2025.

[1] The Chinese general Zhou Enlai famously responded to Henry Kissinger, when asked for his opinion on the French Revolution, ‘It’s too early to say’. In fact, Enlai had thought the question related to the French students’ revolt of 1968.

[2] In local currency.

The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-asset Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund. Performance data provided is either calculated as net or gross of fees as specified. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

Although Troy’s information providers, including without limitation, MSCI ESG Research LLC and its affiliates (the “ESG Parties”), obtain information from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy and/or completeness of any data herein. None of the ESG Parties makes any express or implied warranties of any kind, and the ESG Parties hereby expressly disclaim all warranties of merchantability and fitness for a particular purpose, with respect to any data herein. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein. Further, without limiting any of the foregoing, in no event shall any of the ESG Parties have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2025. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence. Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2025.