Generation Sober? Exploring Youth Drinking Habits

As many of us swap cocktails for mocktails during Dry January, it’s a fitting moment to explore the shifting dynamics of the alcohol industry and what they might mean for our investment in the sector.

Alcoholic beverages are an attractive and resilient consumer category. For instance, Diageo has delivered a ~9% compound annual return since Troy first purchased shares in the company in 2005. Troy also has holdings in Pernod Ricard and Heineken. The companies we favour in the alcohol sector align with the premiumisation trend in drinking behaviours, reflecting a shift towards quality over quantity.

Profits and principles

The sector does however raise questions for responsible investors. The industry profits from the sale of a psychoactive substance that, if abused, poses health and societal challenges. Consumers, investors, and regulators have long known misuse can be harmful. Recently, the US Surgeon General has called for warnings on alcohol bottles. Alcohol misuse is estimated to contribute to 5% of the global disease burden, according to the World Health Organization.

How does investing in alcohol sit within Troy’s responsible investment framework? We are careful to balance risks against opportunities to achieve our investment objective of delivering attractive risk-adjusted returns. Our focus is on the integration of material environmental, social or governance considerations into our investment analysis, this includes staying live to changing consumer preferences and government policymaking.

We do not deem it our role to be the moral arbiters for our investors’ capital. We leave that decision to you by offering alternative portfolios. Our Ethical fund range screens out companies deriving more than 10% revenue from the sale of alcohol. The ethical exclusion criteria of our Ethical portfolios also screens out certain investments in armaments, fossil fuels, gambling, high-interest rate lending, pornography and tobacco[1].

Moderation Matters

“The social licence to operate is not granted by governments or regulators but by the communities and stakeholders impacted by a company’s operations.”

– Ian Thomson, Author

Despite the health-related consequences of excessive alcohol consumption, alcohol remains deeply ingrained in cultural traditions, celebrations, and social connections. Referring to it as a “social lubricant” might raise a few smiles, but anyone who has attended an office party during the festive season can likely appreciate the sentiment. Some may argue that without it, things might get a bit… well, dry.

Notwithstanding this, we believe it is important for alcohol companies to stay vigilant around the risks associated with overconsumption. Failing to do so can harm brand equity and invite regulatory scrutiny. We prefer companies that focus on promoting responsible drinking and thoughtful marketing, which enhances consumer trust and the long-term sustainability of their business models.

The alcohol companies in Troy portfolios focus on premium spirits or beers, prioritising quality over quantity. This strategy creates brand integrity and naturally avoids associations with excessive consumption. Despite this, social risks remain. This prompted us to conduct a focused analysis in 2023 to evaluate how our portfolio companies, Diageo, Pernod Ricard, and Heineken, manage these risks. We summarise their approaches to responsible drinking in the table below, with a focus on marketing practices.

While individual choices matter, alcohol companies play an important role in promoting responsible drinking. We regularly discuss their progress in this area, recognising that addressing social impacts is vital to maintaining their licence to operate.

Secular Decline or Shifting Patterns?

The alcoholic beverages sector has fallen out of investor favour lately, caused by a slowdown in volume growth. This is in stark contrast to the period of exceptional growth seen during and the pandemic, when lockdowns saw consumers ‘pantry-loading’ and up-trading, leading the premium spirits brands to do particularly well. When the world returned to normality, the industry also benefited from a period of ‘revenge conviviality’, as the former Campari CEO called it. This coincided with significant price increases to cover the additional costs of higher input cost inflation and supply chain disruption.

We are now experiencing a hangover from super-normal growth. This softness in quarterly volume figures has led some to extrapolate the effects of what we consider to be a more cyclical slowdown. Many have speculated that depressed volumes is partly caused by a structurally reduced appetite for alcohol consumption by younger consumers and the popularity of GLP-1 weight-loss drugs.

We find that the relationship between trends in alcohol consumption and the growth of GLP-1s is inconclusive. Controlling for other variables, academic studies do not show a clear association between alcohol and obesity. To put it more bluntly than an academic might, obese people aren’t necessarily the biggest drinkers. Furthermore, studies find that two-thirds of patients stop GLP-1 therapy within 24 months and regain over half of their lost weight. Whatever their impact on consumption in the near term, the longer-term impact may be modest unless adherence to these drugs significantly improves. It is ultimately too soon to tell what the long-term impact on demand will be, but early indicators do not suggest that alcohol’s concentrated consumption puts it at an outsized risk from the rise of GLP-1s.

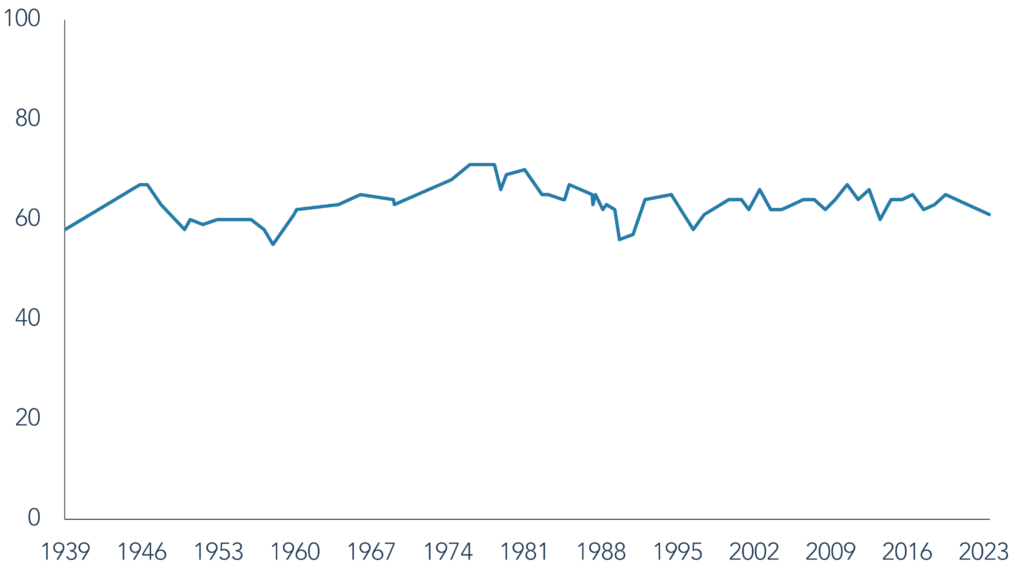

The question of youth drinking habits is also intriguing. If it is true that Gen Z (those born between the late 90s and early 2010s) are drinking less, the alcohol industry may face structural decline. Having researched this topic, we have found that younger demographics are drinking the same quantity of alcohol as generations prior, but they are taking up the habit at an older age than previous generations. The percentage of US adults who drink has consistently fluctuated around the ~60% mark since 1939 and is unchanged in the last 20 years. While it is true that Gen Z drinkers are generally more experimental, more willing to try flavoured spirits and ready-to-drink mixers, for instance, they are not drinking less alcohol.

Figure 1: Percentage of U.S. Adults Who Drink, Trend Since 1939

Source: Gallup, December 2023. 1939-1970 results are based on adults aged 21 and older. 1971-2023 results are based on adults aged 18 and older.

The data also shows that alcohol consumption for 18–25-year-olds has declined but after reaching 25 and transitioning into working adulthood, consumption reverts to historic trends. Drinking prevalence among 25-30-year-olds has remained stable at ~70% since the 1980s, with per capita drinking quantities also staying relatively constant over time.

We suspect the modest decline in consumption for 18–25-year-olds is largely because of the growing economic burden faced by Gen Z. Young Americans graduating with a bachelor’s degree today have a debt-to-income ratio of ~65% compared to ~40% 15 years ago. Additionally, more adults are living at home for economic reasons, leading to fewer opportunities to socialise. Consumer confidence for this demographic is also at an all-time low as this cohort struggle disproportionately with higher costs of living.

Clamping Down on Underage Drinkers

Another notable trend is the reduction in underage drinking. Between 2002-2021, the National Institute on Alcohol Abuse and Alcoholism found that prevalence of alcohol use in the past 30 days among 16 and 17-year-olds dropped by 58%, and by 69% for 14 and 15-year-olds.

This downward trend can be attributed to several factors, including increased awareness of alcohol’s negative effects on adolescent brain development, stricter enforcement of minimum legal drinking age laws, and more effective prevention programmes. In addition, the COVID-19 pandemic contributed to this decline, as school closures and reduced social interactions limited opportunities for underage drinking.

The substantial reduction in underage drinking represents more than just a statistical achievement. While this demographic cohort contributes minimally to alcohol sales, the real victory lies in safeguarding young people until they can make better informed decisions about alcohol consumption when they reach legal age.

Adaptability Wins

While younger demographics exhibit shifting drinking patterns—delaying the start of alcohol consumption and experimenting with newer categories—they are not abandoning alcohol altogether.

These trends underscore the importance of adaptation. Companies that embrace premiumisation, focus on responsible marketing, and anticipate changing preferences are well-positioned for long-term success.

Many of our alcohol companies have launched low and no-alcohol variants, which has been an important source of growth in recent years. Heineken’s low and no-alcohol beers represent over 3% of their global beer volume, whilst Diageo’s Guinness 0.0 has become the UK’s bestselling alcohol-free beer.

The premiumisation trend also has further to go. Authenticity and aspirational consumption remain deeply embedded in consumer behaviours and will continues to shape the industry’s evolution.

The alcohol industry is far from being in structural decline; rather, it is navigating a period of post Covid excess and redefinition. By balancing these issues carefully, we believe the sector can continue to generate attractive returns over the long term.

Whether and whatever you may be drinking this month, we raise a glass to you and wish you a Happy New Year.

[1] For further information on the specific requirements of the ethical exclusion criteria can be found at www.taml.co.uk

[2] Data included in this report is from The University of Michigan Monitoring the Future, The Substance Abuse and Mental Health Services Administration and Bernstein Research

Further information relating to how ESG integration is applied to the fund can be found in the fund prospectus and investor disclosure document. For further information relating to Troy’s approach to company voting and engagement, please see Troy’s Responsible Investment and Stewardship Policy available at www.taml.co.uk. Please refer to Troy’s Glossary of Investment terms here. The document has been provided for information purposes only. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. The document does not have regard to the investment objectives, financial situation or particular needs of any particular person. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The views expressed reflect the views of Troy Asset Management Limited at the date of this document; however, the views are not guarantees, should not be relied upon and may be subject to change without notice. No warranty is given as to the accuracy or completeness of the information included or provided by a third party in this document. Third party data may belong to a third party. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The investment policy and process of the may not be suitable for all investors. Tax legislation and the levels of relief from taxation can change at any time. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy’s information providers, including without limitation, MSCI ESG Research LLC and its affiliates (the “ESG Parties”), obtain information from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy and/or completeness of any data herein. None of the

ESG Parties makes any express or implied warranties of any kind, and the ESG Parties hereby expressly disclaim all warranties of merchantability and fitness for a particular purpose, with respect to any data herein. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein. Further, without limiting any of the foregoing, in no event shall any of the ESG Parties have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. All reference to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2025. ‘FTSE ®’ is a trademark of the London Stock Exchange Group companies and is used by FTSE under licence. Issued by Troy Asset Management Limited (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. © Troy Asset Management Limited 2025