That’s not all, folks

Without wanting to count our chickens too soon, it is natural to reflect on this year’s returns as we edge towards the conclusion of the year. Quite simply, it has been another spectacular year of gains for global equities, and we have again delivered solid results for the Strategy’s investors. The Strategy is up +16% to the end of November, well ahead of many of its peers. This is after making a +24% gain in 2023.

The Strategy’s strong absolute year-to-date returns are less impressive when compared to the global index’s +22% and the S&P 500’s +28%.1 It has been hard for active managers to escape a feeling of inadequacy. When recently introducing his four-year old to Looney Tunes, George easily identified with Daffy Duck who was upstaged by a more muscular rival when he took Melissa Duck to the beach.2

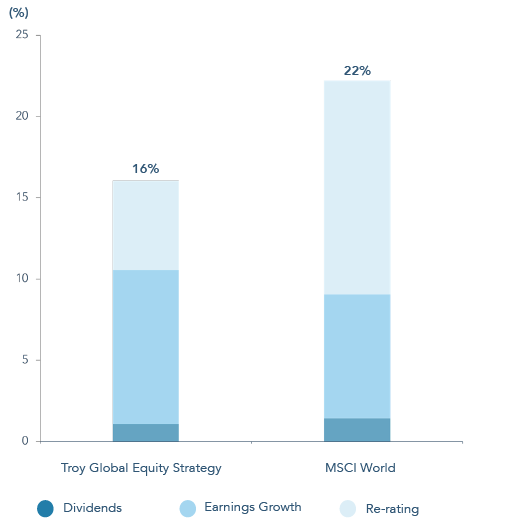

What to make of the divergence of the Strategy’s returns from the market’s? Whilst frustrating to fall behind this year, we are encouraged for two reasons. First, the operating momentum of the Strategy’s underlying companies remains robust. We are pleased that large double-digit gains for longstanding investments including Alcon, American Express (‘Amex’), Booking Holdings and Fiserv, have each been accompanied by double-digit earnings growth. Even where there is some softness (e.g. L’Oréal and LVMH), it is mild and accompanied by significant market share gains. We estimate that earnings and dividend growth have driven about two-thirds of the portfolio’s returns so far this year, whereas the equivalent figure for the market is about 40% (see Figure 1). In other words, the Strategy’s returns in the year to date are comparatively healthy because they are mostly driven by operating results and less dependent on a potentially temporary equity revaluation. Portfolio activity this year also demonstrates our proactive approach to managing risk, including those related to valuation. For instance, the Strategy’s investment in Moody’s was reduced largely on valuation grounds.

Figure 1: Total Return Decomposition YTD

Source: FactSet, 30 November 2024, net of fees. Past performance is not a guide to future performance. Please refer to Troy’s glossary of terms.

Of course, earnings will fluctuate from one year to the next, and we continue to expect the earnings profile of the Strategy’s companies to be steadier than that of the wider market. This feature comes into its own in more difficult markets, when the Strategy tends to outperform. Since its inception at the end of 2013, the Strategy has gained +268% (+12.7% p.a.) compared to the MSCI World Index which is +262% (+12.5% p.a.).

The Strategy’s weighted-average characteristics are the greatest reason for encouragement. They highlight cash margins and capital efficiency are running at well over double the rates of the benchmark index. Our companies have ample opportunities for reinvestment at those high rates of return, and this is resulting in prospective growth rates that are also more than twice that of the global market. And yet the valuation of the portfolio suggests these characteristics are available at a small discount to the market’s own multiples of cashflow. This creates a compelling opportunity, in our view. It gives some confidence in the Strategy’s prospective returns, at least in comparison to the wider market. It also provides some comfort when confronting the many daunting political and economic challenges that undoubtedly lie ahead.

Four more years

In the Strategy’s last Newsletter, published at the start of June, we felt compelled to discuss our views about AI.3 This time it is the re-election of Donald Trump as U.S. President that has propelled markets to new heights. What does Mr Trump’s re-election mean for the Strategy? The normal caveats about the future apply, and whilst the president-elect still awaits inauguration, it is fair to say his last presidency was marked by an unusually large gap between rhetoric and action. With this in mind, we can make a few observations.

The market’s initial positive reaction is eerily similar to the end of 2016. The only difference is Donald Trump is more of a known quantity this time and the market has been faster in cheering his electoral success. The Strategy underperformed in that early phase after the 2016 presidential election when smaller, more domestic, and highly taxed businesses performed best. Performance caught up nicely in subsequent years leading up to the pandemic, outstripping not only the MSCI World, but also the S&P 500. Government policy in the form of tax cuts or tariffs may cause a one-time impact on corporate earnings and investor sentiment, but what really matters to long-term returns is sustainable earnings growth. Our investment time-horizon extends well beyond any presidential term, and we are confident that the forces driving growth for our businesses, including the growing importance of data, cloud computing, AI, and digital payments, are enduring.

With that said, the investment context is much changed since 2016. Valuations and interest rates are in a very different place and share prices already reflect an optimistic ‘no landing’ economic scenario. Trump’s nationalist pro-business agenda and fiscally expansive policies should place upward pressure on inflation and bond yields, which may in turn undermine equity valuations. This calls for valuation discipline.

It is clear that Trump is set to make life harder for importers and overseas manufacturers selling into the U.S. The Strategy is mostly invested in companies selling digital goods and services, which do not easily fit into a mercantilist view of the world. Where the Strategy has limited exposure to companies selling tangible products (e.g. beverages, medical devices), we believe the risks to earnings from higher U.S. tariffs will be manageable through a combination of reshoring, exemptions, and price increases.

More generally, we think there is greater scope for mishaps and unintended consequences under a Trump presidency than under a more moderate leader. This reinforces our preference for a diverse portfolio of financially resilient companies. It also raises the risk of unexpected volatility, making high valuations vulnerable to correction.

A matter of trust

One further aspect of the Trump administration that we are watching closely is the future of regulation. The incoming administration is committed to cutting red tape and this may lessen regulatory oversight for our payments and Big Tech companies, including Alphabet and Visa that face anti-trust cases. Whilst it’s plausible that Amex and other regulated banks will face lower capital requirements, supporting higher shareholder returns, we are not holding our breath for regulatory relief across the portfolio. Influential people on Trump’s team, including the vice-president elect, J.D. Vance, are not fans of Big Tech, and Trump is a particularly vocal opponent of Meta and Mark Zuckerberg. This makes a TikTok ban, for instance, less likely.

We also think that anti-trust cases against Alphabet and Visa are probably too far advanced to be reversed. Alphabet’s U.S. Search case is already so old it was originally filed at the tail end of the last Trump administration. The fact that the case is still unresolved more than four years later is testament to the slow and contentious character of U.S. anti-trust law. Negative headlines in this area will persist for a while, although we wonder if we are at the point of maximum uncertainty in the Alphabet Search dispute. We view the U.S. Department of Justice’s (‘DoJ’) latest demands for a break-up of the company as aggressive positioning in a settlement that leads to more modest change.4 Many of the other proposed remedies are technically challenging, legally dubious, and introduce trade-offs for consumers. We suspect the ruling judge will prefer a settlement more narrowly focused on the issues at hand (Google’s contracts with third-party device manufacturers) rather than risk something more radical that might be overturned on appeal.

Although we are at a much earlier stage with the DoJ’s charges against Visa’s U.S. debit practices (they were first filed in September), our reading of the case and expert feedback raises the likelihood of an early settlement. This is consistent with Visa’s past behaviour, and the company has robust defences to many of the accusations levelled against it. Whatever the outcome, its U.S. debit business is estimated to be a low-teens percentage of Visa’s overall revenues, making any fallout manageable.

We are under no illusion that these anti-trust actions, and others, are in any way good news for these companies. They are costly distractions, posing credible risks to market shares and prospective growth rates at a time when technological change is creating opportunity for rivals. We also believe that it is reasonable to assume Alphabet and Visa maintain leadership positions for many years to come. They aggregate U.S. Search and debit markets with powerful network effects that will likely prove highly resistant to regulatory intervention. The U.S. government is trying to put toothpaste back in the tube. We therefore remain confident that regulatory scrutiny creates opportunity in the shares of these companies. The uncertainty it creates casts a shadow over their strong momentum in other countries and product categories, and neither company has optimised its costs. Alphabet and Visa have ample room to soften any impact on their bottom lines.

Calm, like a duck

In May 1976, a Florida newspaper columnist recorded that Michael Caine described himself as ‘calm, like a duck, on the surface, but paddling like hell underneath’. As fund managers, we sympathise with ‘70s Caine, and ducks generally, even if our long-term perspective, concentrated strategy, and low turnover are deliberately chosen to streamline our efforts.

Whilst educating ourselves on unfolding developments in AI, U.S. politics and regulation, we have been very busy following the progress of the Strategy’s investments. One of our favourite ways to do this is to attend (preferably in person), investor days and events that give a more immersive understanding of our companies’ activities. If quarterly earnings are like taking a shower, investor days are the equivalent of a long, warm bath. Good news for hard-paddling ducks.

This Newsletter is already a long one, so we will limit ourselves to what caught our attention most at the nine events the team has attended in the past three months. We hope it gives investors a flavour of the breadth and dynamic growth that are accessed through the Strategy:

- Adobe (in person) – Adobe MAX, an annual conference for creative professionals, emphasised the stickiness of Adobe’s tools with its (relatively young) users, and the additional value they receive from Adobe’s accelerated innovation, enabled by generative AI. This makes competitive disruption of Adobe’s core creative franchises more apparent than real.

- Experian (online) – Barclay’s Credit Bureau Forum, used by Experian as a proxy for an annual investor day, demonstrated the maturity of the company’s longstanding development of its integrated banking software and consumer platforms. Their scale and continual improvement solidify Experian’s market leadership and underpins accelerated revenue growth and margin expansion.

- Intuit (online) – Intuit’s annual investor day showcased how its far-sighted investments in cloud software and AI have transformed the growth profile of its business by giving them permission to move up-market to disrupt mid-market business software and assisted tax preparation.

- LSEG (online) – A ‘teach-in’ for its clearing business and post-trade services (~15% of group revenues, and one of the many jewels in LSEG’s crown) highlighted how LSEG wins the trust of its customers through the flawless provision of critical market infrastructure and deep partnership with its users. The growth potential of this business is greater than is often perceived.

- Mastercard (in person) – At its first investor day in three years, Mastercard demonstrated the large remaining opportunity in consumer payments, how it is unlocking vast untapped opportunities to capture commercial payment flows, and how its broad service offering wins it market share.

- Novartis (in person) – The annual ‘Meet the Management’ event showed that the company approaches upcoming patent expiries from a position of strength, with great momentum for its newly-launched medicines, improved commercial execution, and a strong mid-to-late-stage R&D pipeline.

- RELX (online) – A seminar focused on its Legal division (~20% of group sales) gave investors a clearer understanding of how analytics and AI are creating substantial value for legal professionals using RELX’s services, supporting enduring and accelerated growth for the division.

- Roche (in person) – The company used its annual R&D Day to outline how it has reformed its governance and practices to apply a more rigorous and efficient framework for managing its R&D.

- Unilever (in person) – An investor event provided an encouraging compendium of all the foundational changes underway at Unilever. Whilst it is early days, greater focus, urgency, and ambition should sustain improved operating performance.

In good company

We recently recorded a podcast episode of Far from the Finishing Post with our colleague, Tom Yeowart. The conversation explores how we work together with the rest of Troy’s investment team, and how the Strategy has evolved. It can be accessed here. We hope you enjoy it.

We wish all our readers a happy and restful end to the year.

1 The global index refers to the MSCI World NR (£).

2 The story also offers hope as Daffy eventually sees off his rival and Melissa takes him back.

3 These continue to hold up well and can be accessed here.

4 A separate anti-trust case focused on Alphabet’s control of advertising technology infrastructure is more likely to result in structural remedies, including divestitures. However, this part of Alphabet has less strategic importance for the company and carries a low share of group profits.

The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Global Equity Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund. Please refer to Troy’s Glossary of investment terms here. Performance data provided is either calculated as net or gross of fees as specified in the relevant slide. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This is a marketing communication document. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Although Troy’s information providers, including without limitation, MSCI ESG Research LLC and its affiliates (the “ESG Parties”), obtain information from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy and/or completeness of any data herein. None of the ESG Parties makes any express or implied warranties of any kind, and the ESG Parties hereby expressly disclaim all warranties of merchantability and fitness for a particular purpose, with respect to any data herein. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein. Further, without limiting any of the foregoing, in no event shall any of the ESG Parties have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any product described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2024.